This is Street Smarts, a column from art advisor Ralph DeLuca that offers art world veterans and newcomers alike a straight-talking, no-bullshit guide to the aloof and difficult-to-crack contemporary art market.

I’m glad to be back writing Street Smarts. Sorry for the long break between columns, but lately my work-life balance seems to be as real as the Easter Bunny. I’ve returned from my hiatus to discuss what I think of as the art world’s 10-K: the 2026 Art Basel & UBS Art Market Report. The annual survey, which tracks global art sales by galleries and at auction, should be taken with a grain of salt. (I have a bunch of questions on how they got and broke down the numbers.) But it’s the best report we have, and even though most people won’t read past the cover page, the data is delivered in a format that would satisfy most money managers.

The report basically confirms what anyone actually writing checks already knows: We aren’t back to the booming market we took for granted coming out of the pandemic, but we are witnessing a reset and repair after three choppy years.

Whether you love it or hate it, art is considered an asset class. It behaves like a store of wealth with measurable financial characteristics—returns, risk, and correlations—distinct from stocks, bonds, or real estate. It goes on your balance sheet and financial institutions are willing to finance, loan, leverage, and fractionalize it.

So you can stick your head in the sand like an ostrich and ignore this reality, or learn how to successfully embrace the numbers before you spend your hard-earned cash on these beautiful and socially relevant assets. The choice is yours. If you choose to at least consider the latter, please read on and indulge my jabs, puns, and theories; they are based on street smart observations and transacting in this field at a high level both personally and on behalf of clients over many years.

Here’s what I’m taking from the report—and what it suggests about where things stand, whether this marks the start of a new cycle or just a dead-cat bounce, and how you can apply these lessons to your own collecting.

The top is back. The middle is lying to itself.

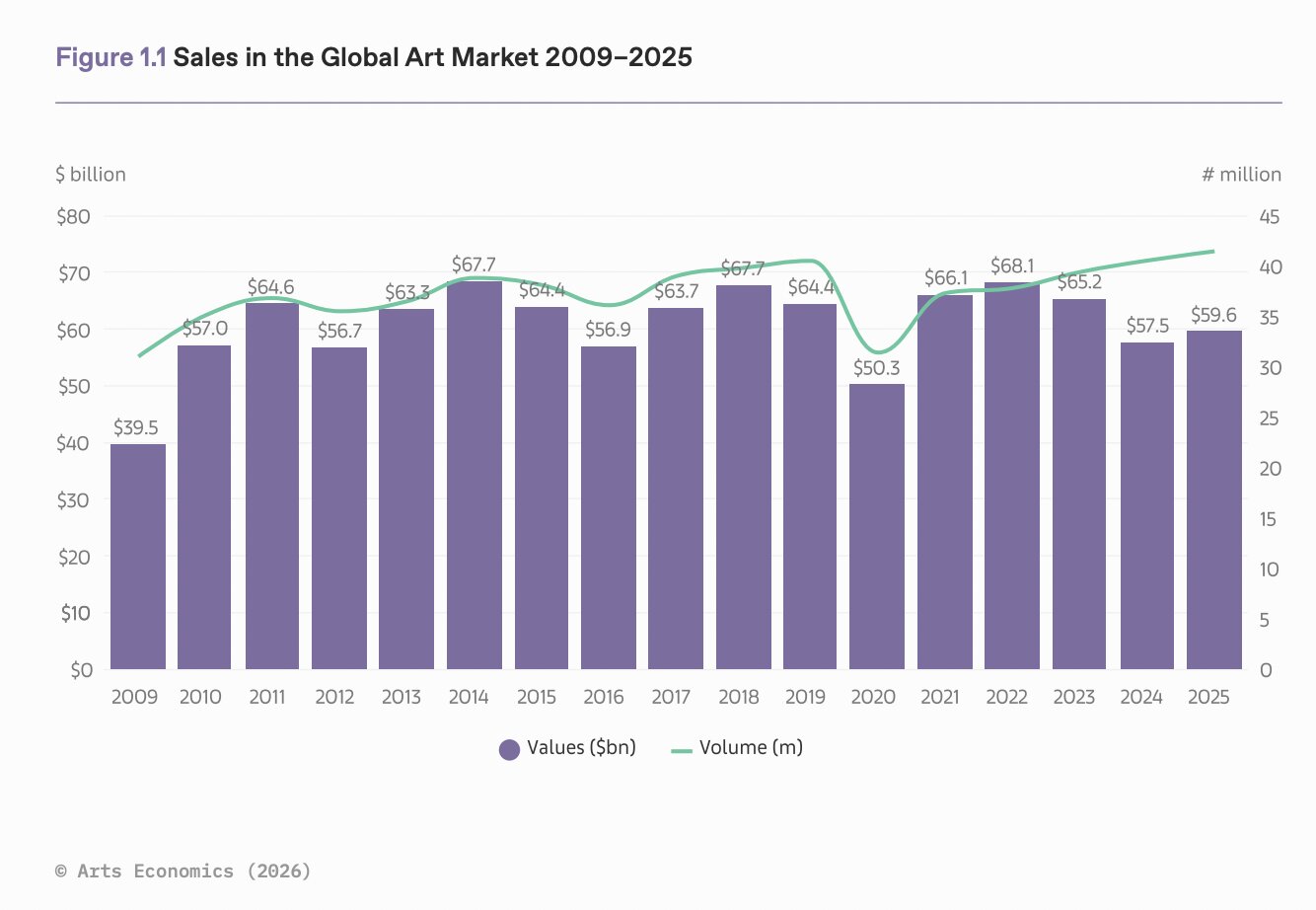

Global art sales in 2025 came in around $59.6 billion (I would still love to know how exactly they came up with that figure—it sounds very high!), up four percent after two down years. On paper, that’s “growth.” In reality, it’s the market dragging itself off the floor—still below the 2022 peak and below 2015 when accounting for inflation.

The number of artworks sold barely budged. We didn’t see a flood of new buyers; instead, we saw more money stacked at the top. At auction, sales of art above $10 million rose 30 percent. The trophy layer is doing the heavy lifting while the rest of the market pretends this is a broad recovery.

If you sit near the high end, this feels “fine.” If you live in the middle, it feels like standing on wet cement and hoping you are able to step away before it dries.

The U.S. is still the biggest arena.

We can all fantasize about gallery shows and art fairs in exotic places and bullshit ourselves that we need to spend top dollar to fly to these playgrounds of the wealthy. But the U.S. is still the main stage: It represented roughly 44 percent of global art sales (about $26 billion dollars in 2025), up 5 percent after two ugly years.

You don’t get that large a market share without issues. Last year was defined by tariff threats, toxic tweets, reversals, political turmoil, doomsday-inspired headlines, and multiple gallery closures.

Imports of art and antiques into the U.S. climbed, exports slipped, and everyone in the market felt the same thing: The art is fine, but the rules governing the trade are volatile.

If you’re actually deploying seven‑ and eight‑figure capital, you treat the U.S. like a blue chip stock: incredible liquidity, real upside, and totally tied to policy tantrums. You don’t avoid the market, but you do have to price in the risk.

Online is the funnel, not the throne.

The Covid fantasy was that the art market had “finally gone digital.” 2025 killed that delusion.

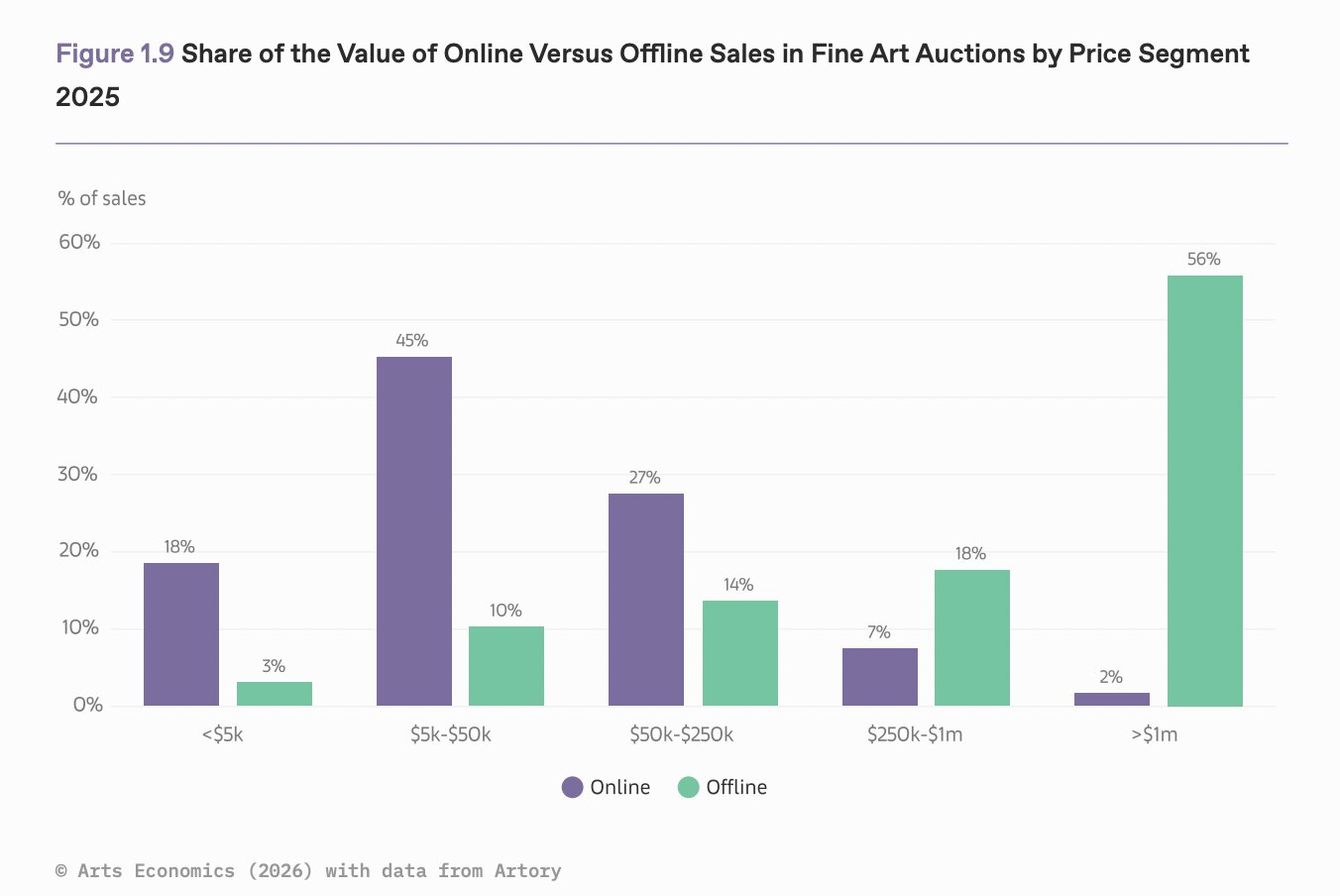

Online‑only sales dropped to around $9.2 billion, about 15 percent of the total market, down from 25 percent at the 2020 peak. That’s still higher than pre‑Covid, but the trend is obvious: People want to look a painting in the eye again. AS THEY SHOULD!

The price profile outlines how things have shifted. Offline, the largest value is in the $1 million-plus price bracket. Online, sales are dominated by pieces under $50,000.

You should use the web for what it actually does well.

- It’s your research portal for news, auction prices, and market research, as well as alerts for what auctions and lots are coming up in the near future.

- It’s where you might first see a new artist, move lower and mid‑priced works, and keep the machine running between fairs and big sales.

- It’s where galleries and collectors make contact for the first time. Dealers reported that 40 percent of their total online sales last year were to first-time buyers. A gallery’s website is its new front door.

When a work is reputationally or financially serious, however, it is still selling in a room, not a browser. Anyone still preaching that the future of art is “100 percent online” is either selling you software or a Substack subscription to their so-called market insights.

Many I would bet have never spent real money on a painting, or directed a client to do so. We should normalize asking advisors and “gurus”— especially the ones who are usually pushing the narrative that online is the future of the art market—what they personally own and what sort of things they are actually getting paid to advise people to buy.

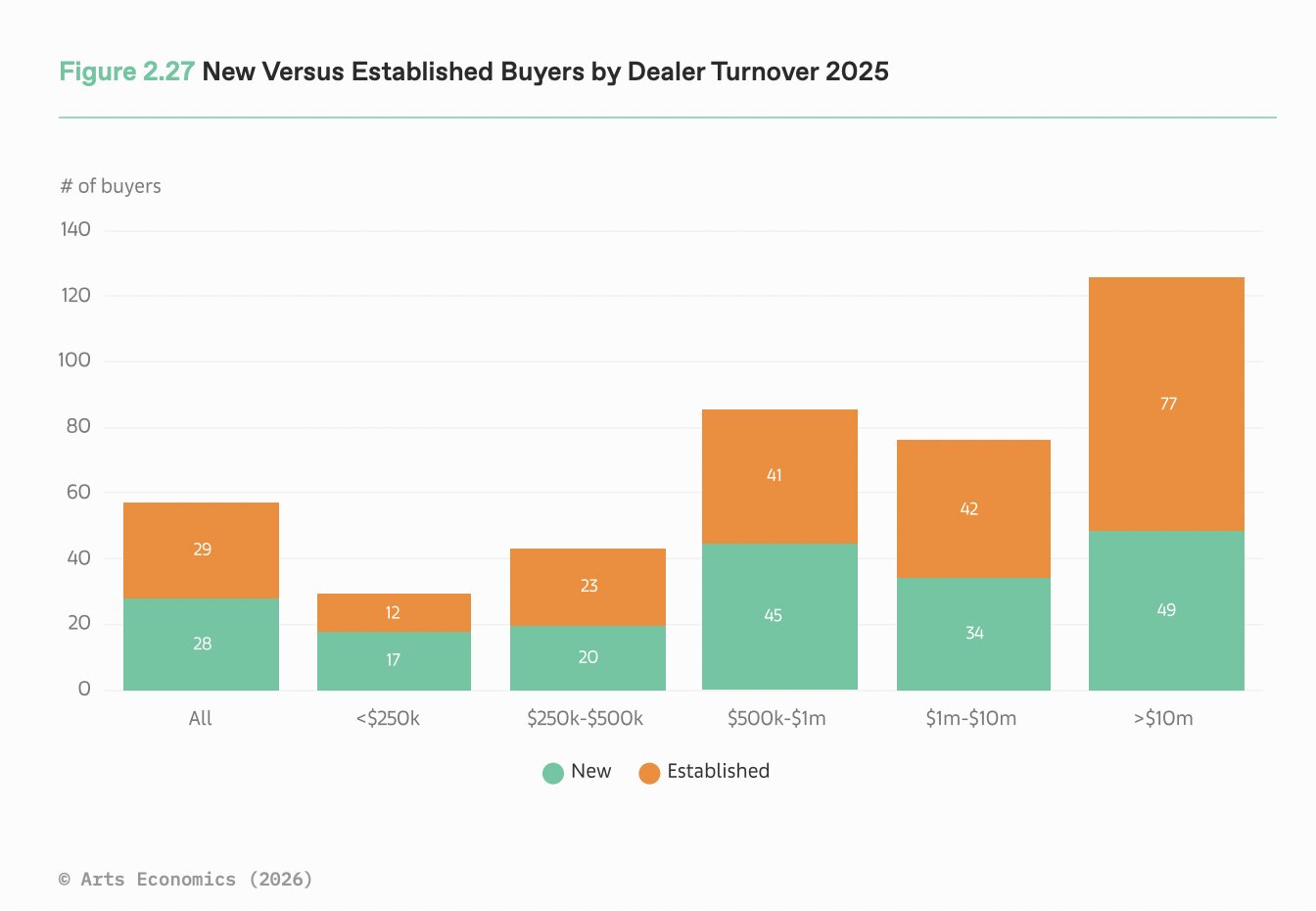

Dealers: first‑class rent, economy‑class margins.

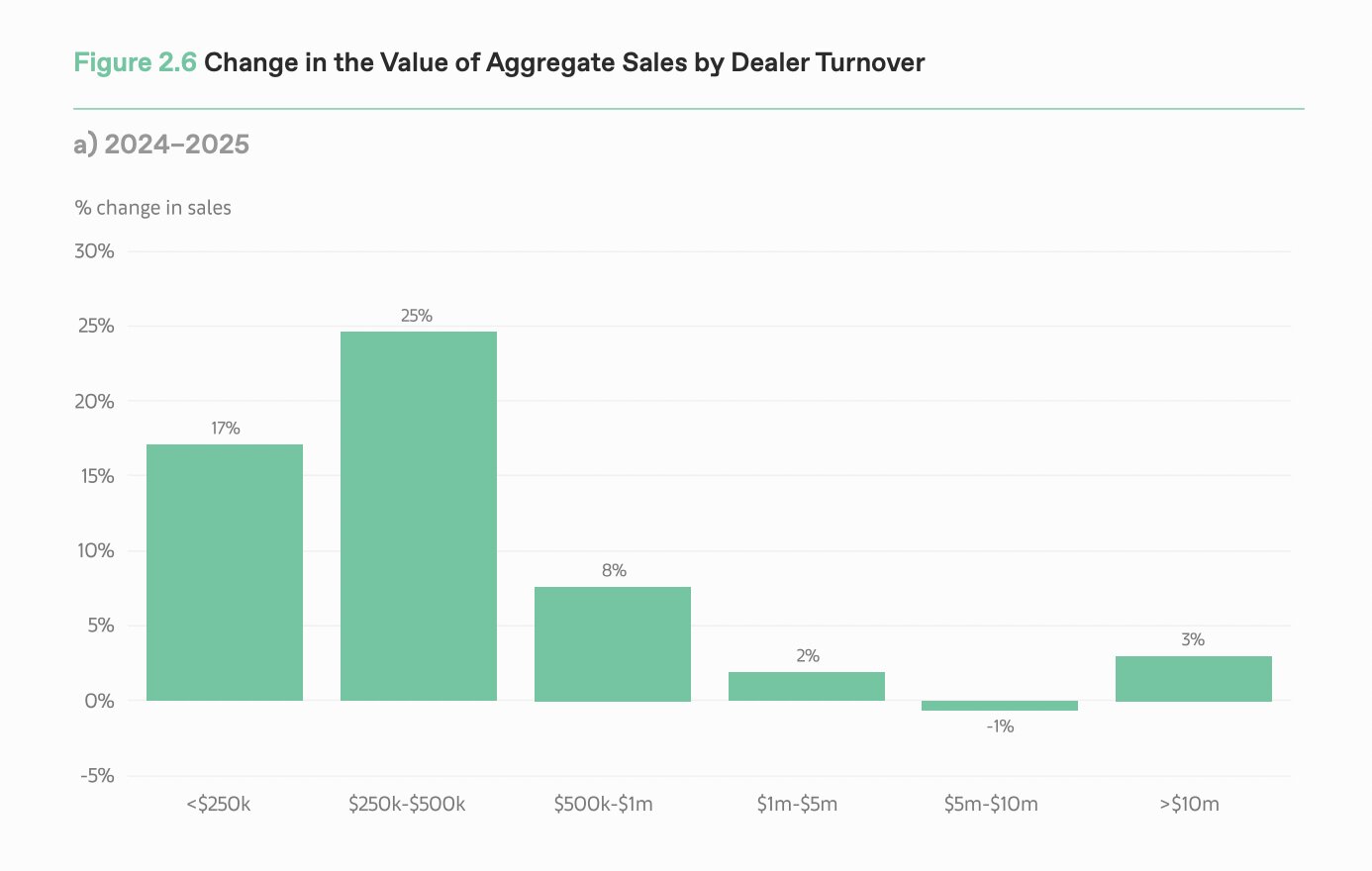

Dealer sales crawled up to about $34.8 billion last year, a two percent rise that feels less like a win than a way to keep the lights on.

The structure is pure barbell:

- Small dealers grew fast in percentage terms (those with turnover of between $250,000 and $500,000 saw sales rise 25 percent). They are lean, local, flexible, without bloated overhead.

- The big boys ($10 million‑plus turnover) got back in the black to access: top inventory, top collectors, top brand. But their growth was thinner: 3%.

- The mid‑tier shops with $1 million to $10 million in annual sales are the ones in trouble: sales are flat, costs are up, and way too much money is tied up in square footage, fairs, and aging inventory. Those with an average turnover of $5 million to $10 million saw sales shrink by one percent.

This group—the one with first‑class rent and economy‑class margins—will be punished most harshly. When logistics, shipping, insurance, fairs, and travel costs all climb faster than sales, mega-galleries can absorb the shock and push it through to clients. The mid-tier can’t.

But don’t get alarmist: Galleries are not “dying.” The data show that openings still outnumber closures. What’s dying is the lazy gallery model: too many fairs, no data, a couple of whales paying for an entire year.

Fewer clients, bigger dependency.

This brings me to one of the quieter shifts in the market. Galleries are relying on fewer and fewer buyers, especially at the lower end. In 2025, a gallery’s average number of clients dropped substantially to 57, the lowest average since 2021, according to the report. Small galleries are increasingly living off an even shorter list of collectors. This matters because, as I have said many times, small galleries and the emerging artists they specialize in are essential to keeping the whole market alive and well. Younger galleries cultivate new artistic talent and a new generation of collectors. As their income grows, so will their buying and patronage!)

The reliance on a few major buyers is concentration risk in human form. If two of your main collectors get divorced, change advisors, or move on to watches and wine, your P&L will feel it.

The dealers who survive this phase will treat their client book like a portfolio: diversify, constantly bring in new collectors at the entry tier, and never let three people decide whether you eat.

Gender: culture moved faster than money. That’s your edge.

On gender, the optics have improved. Gallery rosters are much closer to parity (41 percent, up from 32 percent in 2018); in the primary market, they are pretty much equal .

Sales are where you see the lag. Women artists still take a smaller share of total sales (37 percent) than their share of representation (45 percent), and that gap widens as you move up into the highest‑turnover galleries.

So yes, it’s structural inequality. But let’s stay honest: It’s also a pricing mistake.

If the top of the market is still underpaying women relative to the quality of their representation and level of demand, smart collectors will quietly lean in while everyone else is still focused on panel discussions.

Style shift: hype is out, heritage is back.

The post‑Covid trade was all about “ultra‑contemporary”—fresh names, fast flips, auction records for paintings that were still wet. We all know how that ended.

Sales by contemporary art dealers were stagnant in 2025. At auction, the number of works created in the last 20 years that sold for over $1 million fell by almost a third. The energy has shifted to the stability of:

- Established postwar names

- Modern art

- Parts of Impressionist and Old Masters that were left for dead while everyone chased 29‑year‑olds with neon palettes

This is the art‑world version of rotating from speculative growth into quality. People didn’t fall out of love with new art; they just remembered what risk feels like. You can’t sell an artwork for seven or eight figures on a strong narrative anymore.

You need museum backing, institutional shows, and a track record of staying power.

Taxes and Tariffs and A.I., oh my!

The boring stuff—ever-changing taxes, tariffs, cultural‑goods rules, extra paperwork, and A.I. labels—is no longer a footnote. Over half of dealers (56 percent) said that tariffs negatively affected business and the report estimates that rising costs for dealers outpaced inflation at 5 percent.The headline is simple: The friction tax went up.

- More paperwork

- More inspections

- More intermediaries between you and the work

- More regulation around A.I.: mandatory labels for A.I.‑generated images, artists pushing back on training data, and big questions about the long‑term rights and value of purely machine‑generated work

- More chances for a shipment to get held up because someone, somewhere, doesn’t like a classification code

Every extra rule increases the time and money spent. If you’re not taking that into account at this point, I don’t know what to tell you.

How to actually play this phase

If you’re treating art like an actual asset class, not just a hobby, consider this my operating manual:

- Lean into the high end, but assume policy changes can hit your shipping, your timing, and your exits. Price that in from day one.

- Avoid galleries with taste and no discipline. If they’re living off two collectors, that’s not a partner, that’s counterparty risk.

- Go online to research price history and upcoming auctions, not to find the next art trend or make serious purchases.

- Look where culture has moved faster than money—women artists, certain regions, older sectors quietly coming back. That’s where the mispricing hides.

Everyone else will just quote the top ten auction results and repost fair photos. The edge goes to the people who read these kinds of reports the way traders read earnings reports—looking to capitalize on the places where the story and the numbers don’t line up.

My gut is we are in for a terrific auction season in New York in May with many pedigreed collections and trophy items hitting the auction block. Until next time, stay informed, stay curious, and call out the bullshit!

DeLuca’s Definitions: An Art-World Glossary

10-K of the Art Market

The corporate 10-K is an SEC-mandated, audited breakdown of a company’s financial reality and the most reliable, standardized source of truth investors get. The 2026 Art Basel & UBS Art Market Report is the closest the art world gets to that level of insight, minus the audits. However, unlike a real 10-K, it’s part hard numbers, part educated guesswork, and part narrative management.

Barbell Market

A market where strength is concentrated at the high and low ends, while the middle gets squeezed.

Counterparty Risk

The probability that the other party in a financial transaction—such as a trade, loan, or derivative contract—defaults or fails to meet their contractual obligations. Essentially, the risk that the other side of a deal fails to deliver.

High-Beta Market

A market with strong upside but heightened sensitivity to external forces (policy, tariffs, sentiment).

Trophy Layer

The ultra-high-end segment (greater than $10 million) that disproportionately drives total market value.

Whale Dependency

When a dealer’s business relies heavily on a handful of top buyers.

More of our favorite stories from CULTURED

How Blue Ribbon Survived a Mob Run-in and Transformed Late-Night Dining

Why Cookbooks Are the Next Frontier for Narrative Writing

You’ve Heard About the New Museum’s New Building. The New Show Is Even Better.

Everyone Was Afraid to Touch Nadav Lapid’s Satire of Israeli Artists. Now, It’s Being Released.

Where 27 Artists Are Hanging Out in New York Right Now

Sign up for our newsletter here to get these stories direct to your inbox.

in your life?

in your life?